DRS/A: Draft registration statement submitted by Emerging Growth Company under Securities Act Section 6(e) or by Foreign Private Issuer under Division of Corporation Finance policy

Published on February 9, 2024

Table of Contents

As confidentially submitted with the Securities and Exchange Commission on February 9, 2024

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 2

TO

CONFIDENTIAL DRAFT SUBMISSION

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Loar Holdings, LLC

to be converted as described herein to a corporation named

Loar Holdings Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 3728 | 82-2665180 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification No.) |

20 New King Street

White Plains, New York 10604

(914) 309-1311

(Address, including zip code, and telephone number, including area code, of registrants principal executive offices)

Dirkson Charles

President, Chief Executive Officer and Executive Co-Chairman

Loar Holdings, LLC

20 New King Street

White Plains, New York 10604

(914) 309-1311

(Name, address, including zip code, and telephone number, including area code, of registrants agent for service)

With copies to:

| Sean T. Peppard Aslam A. Rawoof Benesch, Friedlander, Coplan & Aronoff LLP 1155 Avenue of the Americas, Floor 26 New York, New York 10036 (646) 593-7050 |

Michael Manella Vice President, General Counsel and Secretary Loar Holdings, LLC 20 New King Street White Plains, New York 10604 (914) 309-1311 |

Craig E. Marcus Tara Fisher Ropes & Gray LLP Prudential Tower 800 Boylston Street Boston, Massachusetts 02199 (617) 951-7000 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement is declared effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box: ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of large accelerated filer, accelerated filer smaller reporting company and emerging growth company in Rule 12b-2 of the Exchange Act:

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||

| Non-accelerated filer | ☒ | Smaller reporting company | ☐ | |||

| Emerging growth company | ☒ | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until this Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities nor a solicitation of an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED , 2024

PRELIMINARY PROSPECTUS

Shares

LOAR HOLDINGS INC.

Common Stock

This is Loar Holdings Inc.s initial public offering of our common stock (common stock). We are offering shares of common stock. Prior to this offering, there has been no public market for our common stock. We expect that the initial public offering price of our common stock will be between $ and $ per share. We intend to apply to list our common stock on the under the symbol LOAR.

See Risk Factors beginning on page 18 to read about factors you should consider before buying shares of our common stock.

We are an emerging growth company as defined in Section 2(a)(19) of the Securities Act of 1933, as amended (the Securities Act), and, as such, we have elected to comply with certain reduced public company reporting requirements for this prospectus and may elect to do so in future filings.

Neither the Securities and Exchange Commission (the SEC) nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

| Per share | Total | |||||||

| Initial public offering price |

$ | $ | ||||||

| Underwriting discounts and commissions(1) |

$ | $ | ||||||

| Proceeds, before expenses, to us |

$ | $ | ||||||

| (1) | See Underwriting for additional information regarding underwriting compensation. |

We have granted the underwriters the right, for a period of 30 days from the date of this prospectus, to purchase up to additional shares of common stock from us at the initial public offering price less the underwriting discount.

The underwriters expect to deliver the shares to purchasers on , 2024.

| Jefferies | Morgan Stanley |

| Moelis & Company |

, 2024

Table of Contents

| Page | ||||

| 1 | ||||

| 18 | ||||

| 42 | ||||

| 44 | ||||

| 45 | ||||

| 46 | ||||

| 47 | ||||

| 49 | ||||

| Managements Discussion and Analysis of Financial Condition and Results of Operations |

51 | |||

| 64 | ||||

| 74 | ||||

| 82 | ||||

| 85 | ||||

| 88 | ||||

| 91 | ||||

| 98 | ||||

| Certain United States Federal Income Tax Consequences to Non-U.S. Holders |

100 | |||

| 105 | ||||

| 114 | ||||

| 114 | ||||

| 114 | ||||

| F-1 | ||||

Through and including the 25th day after the date of this prospectus, all dealers that effect transactions in these shares of common stock, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to the dealers obligations to deliver a prospectus when acting as underwriters and with respect to their unsold allotments or subscriptions.

You should rely only on the information contained in this prospectus or in any free writing prospectus we may authorize to be delivered or made available to you. Neither we nor the underwriters have authorized anyone to provide you with different information. Neither we nor any of the underwriters take any responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. The information in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus, or any free writing prospectus, as the case may be, or any sale of shares of our common stock. Our business, results of operations and financial condition may have changed since such date.

For investors outside the United States: we are offering to sell, and seeking offers to buy, shares of our common stock only in jurisdictions where offers and sales are permitted. Neither we nor any of the underwriters have done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than in the United States. Persons outside the United States who come into possession of this prospectus must inform themselves about, and observe any restrictions relating to, the offering of the shares of common stock and the distribution of this prospectus outside the United States.

i

Table of Contents

BASIS OF PRESENTATION

Loar Holdings, LLC, the registrant whose name appears on the cover of this registration statement, is a Delaware limited liability company. Immediately prior to the effectiveness of this registration statement, Loar Holdings, LLC will convert into a Delaware corporation pursuant to a statutory conversion and will change its name to Loar Holdings Inc. We refer to this conversion throughout the prospectus included in this registration statement as the Corporate Conversion. As a result of the Corporate Conversion, Loar Acquisition 13, LLC, the sole unitholder of Loar Holdings, LLC, will become the sole holder of shares of common stock of Loar Holdings Inc. Upon the consummation of this offering, LA 13 will distribute the shares of common stock of Loar Holdings Inc. to its members and then liquidate immediately thereafter in accordance with applicable law. See Certain Relationships and Related Party TransactionsLA 13 LLC Agreement. Except as disclosed in the prospectus, the consolidated financial statements and related notes thereto and other financial information included in this registration statement are those of Loar Holdings, LLC and its subsidiaries and do not give effect to the Corporate Conversion. Shares of common stock, par value $ per share, of Loar Holdings Inc. are being offered by the prospectus that forms a part of this registration statement.

We will be a holding company and, upon consummation of this offering and the application of net proceeds therefrom, our sole asset will be the capital stock of our wholly owned subsidiaries, including Loar Group, Inc. Loar Holdings, LLC will be the predecessor of the issuer for financial reporting purposes. Accordingly, this prospectus contains the historical financial statements of Loar Holdings, LLC and its consolidated subsidiaries. Loar Holdings Inc. will be the reporting entity following this offering.

INDUSTRY AND MARKET DATA

Within this prospectus, we reference information and statistics regarding the industry in which we operate. We have obtained this information and statistics from various independent third-party sources, independent industry publications, reports by market research firms and other independent sources. Some data and other information contained in this prospectus are also based on managements estimates and calculations, which are derived from our review and interpretation of internal surveys and independent sources. The information is as of its original publication dates (and not as of the date of this prospectus). Data regarding the industries in which we compete and our market position and market share within these industries are inherently imprecise and are subject to significant business, economic and competitive uncertainties beyond our control, but we believe they generally indicate size, position and market share within these industries. We are responsible for all of the disclosure in this prospectus and believe the third-party information and our internal company research, data and estimates contained in this prospectus to be reliable, neither have we independently verified any third-party information nor has any independent source verified our internal company research, data and estimates.

In addition, assumptions and estimates of our and our industrys future performance are subject to a high degree of uncertainty and risk due to a variety of factors, including those described in Risk Factors. These and other factors could cause our future performance to differ materially from our assumptions and estimates. See Cautionary Note Regarding Forward-Looking Statements. As a result, you should be aware that market, ranking, and other similar industry data included in this prospectus, and estimates and beliefs based on that data may not be reliable. Neither we nor the underwriters can guarantee the accuracy or completeness of any such information contained in this prospectus.

TRADEMARKS, SERVICE MARKS, TRADENAMES, AND COPYRIGHTS

We own a number of registered and common law trademarks and pending applications for trademark registrations in the United States. Unless otherwise indicated, all trademarks, service marks, trade names, and copyrights appearing in this prospectus are proprietary to us, our affiliates, and/or licensors. This prospectus also contains trademarks, tradenames, service marks, and copyrights of third parties, which are the property of their respective owners. Solely for convenience, the trademarks, tradenames, service marks, and copyrights referred to

ii

Table of Contents

in this prospectus may appear without the ®, TM, SM, or © symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or the rights of the applicable licensors to these trademarks, tradenames, service marks, and copyrights. We do not intend our use or display of other parties trademarks, tradenames, service marks, or copyrights to imply, and such use or display should not be construed to imply, a relationship with, or endorsement or sponsorship of us by, these other parties.

NON-GAAP FINANCIAL MEASURES

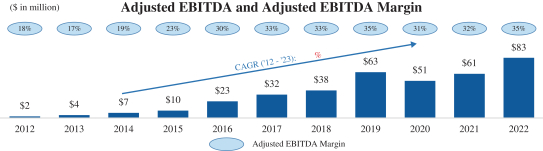

We present certain financial information based on our EBITDA, Adjusted EBITDA and Adjusted EBITDA Margin. References to EBITDA mean earnings before interest, taxes, depreciation and amortization, references to Adjusted EBITDA mean EBITDA plus, as applicable for each relevant period, certain adjustments as set forth in the reconciliations of net loss to EBITDA and Adjusted EBITDA and references to Adjusted EBITDA Margin refer to Adjusted EBITDA divided by net sales. EBITDA, Adjusted EBITDA and Adjusted EBITDA Margin, are not measurements of financial performance under U.S. GAAP. We present EBITDA, Adjusted EBITDA and Adjusted EBITDA Margin, because we believe they are useful indicators for evaluating operating performance. In addition, our management uses Adjusted EBITDA to review and assess the performance of the management team in connection with employee incentive programs and to prepare its annual budget and financial projections. Moreover, our management uses Adjusted EBITDA of target companies to evaluate acquisitions.

Although we use EBITDA, Adjusted EBITDA and Adjusted EBITDA Margin, as measures to assess the performance of our business and for the other purposes set forth above, the use of non-GAAP financial measures as analytical tools has limitations, and you should not consider any of them in isolation, or as a substitute for analysis of our results of operations as reported in accordance with U.S. GAAP. Some of these limitations are:

| | EBITDA, Adjusted EBITDA and Adjusted EBITDA Margin, do not reflect the significant interest expense, or the cash requirements, necessary to service interest payments on our indebtedness; |

| | although depreciation and amortization are non-cash charges, the assets being depreciated and amortized will often have to be replaced in the future, and the cash requirements for such replacements are not reflected in EBITDA, Adjusted EBITDA and Adjusted EBITDA Margin; |

| | EBITDA, Adjusted EBITDA and Adjusted EBITDA Margin, exclude the cash expense we have incurred to integrate acquired businesses into our operations, which is a necessary element of certain of our acquisitions; |

| | the omission of the substantial amortization expense associated with our intangible assets further limits the usefulness of EBITDA, Adjusted EBITDA and Adjusted EBITDA Margin; and |

| | EBITDA, Adjusted EBITDA and Adjusted EBITDA Margin, do not include the payment of taxes, which is a necessary element of our operations. |

Because of these limitations, EBITDA, Adjusted EBITDA and Adjusted EBITDA Margin, should not be considered as measures of cash available to us to invest in the growth of our business. Management compensates for these limitations by not viewing EBITDA, Adjusted EBITDA and Adjusted EBITDA Margin, in isolation and specifically by using other U.S. GAAP measures, such as net sales and operating profit, to measure our operating performance. EBITDA, Adjusted EBITDA and Adjusted EBITDA Margin, are not measurements of financial performance under U.S. GAAP, and they should not be considered as alternatives to net loss or cash flow from operations determined in accordance with U.S. GAAP. Our calculations of EBITDA, Adjusted EBITDA and Adjusted EBITDA Margin, may not be comparable to the calculations of similarly titled measures reported by other companies. For a reconciliation of net loss to EBITDA, Adjusted EBITDA and Adjusted EBITDA Margin, for the years ended December 31, 2022 and December 31, 2023, see Managements Discussion and Analysis of Financial Condition and Results of OperationsNon-GAAP Financial Measures.

iii

Table of Contents

CERTAIN DEFINITIONS

As used in this prospectus, unless the context otherwise requires, the Company, our company, Loar, we, us and our refer to Loar Holdings, LLC and its consolidated subsidiaries for all periods prior to the Corporate Conversion discussed below and to Loar Holdings Inc. and its consolidated subsidiaries for all periods following the Corporate Conversion. In addition, as used in this prospectus, unless the context otherwise requires:

| | Board refers to our board of directors; |

| | CAGR refers to compound annual growth rate; |

| | CAV refers to CAV Systems Group Limited; |

| | Credit Agreement refers to our Credit Agreement, dated as of October 2, 2017, by and among Loar Group, Inc., Loar Holdings, LLC, the other guarantors party thereto from time to time, the lenders party thereto from time to time and First Eagle Alternative Credit, LLC, as administrative agent (the Administrative Agent) for the lenders and as collateral agent for the secured parties, as amended, restated, supplemented or otherwise modified (including as of June 30, 2023); |

| | DAC-EP refers to DAC Engineered Products, LLC; |

| | Delayed Draw Term Loans refers to the meaning assigned to such term in the Credit Agreement; |

| | DGCL refers to Delaware General Corporation Law; |

| | Exchange Act refers to the Securities Exchange Act of 1934, as amended; |

| | FAA refers to the Federal Aviation Administration in the United States; |

| | GAAP refers to U.S. generally accepted accounting principles; |

| | JLL refers to JLL Partners; |

| | K&F refers to K&F Industries; |

| | LA 13 refers to Loar Acquisition 13, LLC, a Delaware limited liability company, which will liquidate in accordance with applicable law immediately following the occurrence of this offering and the distribution described in Certain Relationships and Related Party TransactionsLA 13 LLC Agreement; |

| | LIBOR refers to the London Interbank Offered Rate; |

| | LLC Agreement refers to the Fifth Amended and Restated Limited Liability Company Agreement of LA 13; |

| | McKechnie refers to McKechnie Aerospace; |

| | OEMs refers to original equipment manufacturers; |

| | Principal Stockholders refers to ; |

| | Revenue Passenger Kilometers and RPKs refer to revenue paying passengers multiplied by the distance travelled in kilometers; |

| | Revolving Line of Credit refers to the revolving line of credit under the Credit Agreement; |

| | Sarbanes-Oxley Act refers to the Sarbanes-Oxley Act of 2002, as amended; |

| | SOFR refers to the Adjusted Term Secured Overnight Financing Rate; and |

| | TransDigm refers to TransDigm Group Incorporated. |

iv

Table of Contents

This summary highlights information contained elsewhere in this prospectus. This summary may not contain all the information that may be important to you. You should carefully read the entire prospectus before making an investment decision, including the information presented under the heading Risk Factors, Managements Discussion and Analysis of Financial Condition and Results of Operations and the financial statements and related notes included elsewhere in this prospectus.

Our Company

We specialize in the design, manufacture, and sale of niche aerospace and defense components that are essential for todays aircraft and aerospace and defense systems. Our focus on mission-critical, highly engineered solutions with high-intellectual property content resulted in approximately % of our 2023 net sales being derived from proprietary products where we believe we hold market-leading positions. Furthermore, our products have significant aftermarket exposure, which has historically generated predictable and recurring revenue. We estimate that approximately % of our 2023 net sales were derived from aftermarket products.

The products we manufacture cover a diverse range of applications supporting nearly every major aircraft platform in use today and include auto throttles, lap-belt airbags, two- and three-point seat belts, water purification systems, fire barriers, polyimide washers and bushings, latches, hold-open and tie rods, temperature and fluid sensors and switches, carbon and metallic brake discs, fluid and pneumatic-based ice protection, RAM air components, sealing solutions and motion and actuation devices, among others. We primarily serve three core end markets: commercial, business jet and general aviation, and defense, which have long historical track records of consistent growth. We also serve a diversified customer base within these end markets where we maintain long-standing customer relationships. We believe that the demanding, extensive and costly qualification process for new entrants, coupled with our history of consistently delivering exceptional solutions for our customers, has provided us with leading market positions and created significant barriers to entry for potential competitors. By utilizing differentiated design, engineering, and manufacturing capabilities, along with a highly targeted acquisition strategy, we have sought to create long-term, sustainable value with a consistent, global business model.

Our ability to deliver high-quality solutions stems from managements extensive industry experience and their long history of creating value across multiple businesses. Prior to the formation of Loar, Chief Executive Officer and Co-Chairman Dirkson Charles, Chief Financial Officer Glenn DAlessandro, and VP & General Counsel Michael Manella helped lead K&F through 17 years of sustained success, including its initial public offering and ultimate sale to Meggitt plc (now part of Parker-Hannifin Corporation). The team, building upon its proven ability to create value, subsequently worked together at McKechnie until its 2010 sale to TransDigm. During their tenure at McKechnie, they worked alongside the Companys Co-Chairman Brett Milgrim, who was a Managing Director and Partner of JLL, McKechnies majority owner before the sale to TransDigm. Through their collective experience at K&F and McKechnie, the management team built deep industry expertise and harnessed this knowledge to launch Loar, even entering some of the same product categories as K&F and McKechnie such as carbon and metallic brake discs, hydraulic valves, keepers, rate control devices, latches, hold-open rods, starter generators, and actuators, among others. By having the advantage of a clean blueprint and targeted list of attractive product categories and acquisition candidates, the management team has been able to leverage its significant experience to create a purpose-built, successful platform.

Loar is centered around a commitment to a consistent and focused business modelcreating a portfolio of proprietary products serving a highly diverse set of applications, end markets and customers within the aerospace and defense value chain. This strategy has resulted in what we believe to be market-leading positions, driven by products that have been difficult for competitors to replicate. The qualification process for

1

Table of Contents

the Companys products serves as a significant barrier to entry for new suppliers. The time, investment, and risks associated with qualification are substantial. The process can often take years, involving multiple tests that require support and financial contribution from both the system supplier and the OEM. Moreover, the Company focuses on products that make up a relatively small portion of the total cost of an aircraft. As a result, it is not typically economical for OEMs to repeat the process of qualification after an existing supplier has been qualified already onto a given aircraft platform. In addition, customer relationships represent a key barrier to entry. Given the mission-critical nature of the Companys products, we believe our customers look for highly reliable suppliers they can trust to deliver on-time, high-quality solutions. Loars position as a trusted supplier of highly engineered, value-added products not only has created significant barriers to entry, but also has established an ability to fairly value our products, which has resulted in consistent improvements to Loars gross profit margins over the long-term.

Our portfolio of products serves a variety of applications across aircraft platforms as shown below:

Once Loars components are qualified on an aircraft platform, we believe we are likely to maintain our position as the provider of aftermarket parts and services for the life of the platform and related platform derivatives. This results in significant aftermarket revenue, which represented % of our 2023 net sales. For the platforms we serve, the total life of an aircraft can be up to 50 years, ensuring steady aftermarket revenue streams with historically higher margins than revenue to OEM customers. We believe our aftermarket exposure provides us with an opportunity for stable, recurring, long-lasting and high-margin financial performance.

In addition to our OEM and aftermarket balance, our revenue is diversified across end markets, customers, and platforms. No more than % of our 2023 net sales came from any single customer, and no more than % of our 2023 net sales came from any single aircraft platform. We believe that our revenue diversification provides significant resiliency, and it positions us well to take advantage of new business opportunities.

| 2023 Net Sales by End Market |

2023 Net Sales by Consolidated Customer |

2023 Net Sales Composition |

Top 6 Aircraft of 2023 Net Sales |

2

Table of Contents

We believe that our efforts to serve our customers effectively have also differentiated our business and led to long-standing customer relationships. Given the complexity of our customers supply chains, they look for dependable suppliers across multiple products and capabilities. In addition to providing a broad set of capabilities, we believe our commitment to quality, consistent on-time delivery and highly specialized tailored solutions furthers our long-standing relationships. Our relationships enable an open dialogue regarding our customers supply chain challenges, which can give us insight into potential growth opportunities, both organically and inorganically.

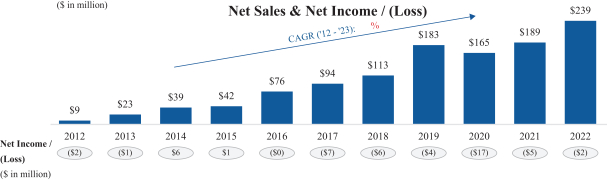

In 2023, we generated $ million in net sales. Since the inception of our Company in 2012, we have grown our net sales at a CAGR of % . We generated a GAAP reported net loss of $ million in 2023 and $ million in Adjusted EBITDA in 2023, representing a GAAP reported net loss margin of % and a % Adjusted EBITDA margin. Including one-time investments of $ million related to the relocation of a manufacturing facility and the construction of a new factory in 2023, we invested $ million in capital expenditures in 2023. Our historical capital expenditures from 2012 to 2023 have averaged % of net sales, highlighting the low capital requirements of our business model. Over the next 12 months, we expect our capital needs to be in-line with previous years at approximately % of net sales. For a discussion of the use of Adjusted EBITDA and Adjusted EBITDA Margin, and a reconciliation to the most directly comparable GAAP measures, see Managements Discussion and Analysis of Financial Condition and Results of OperationsNon-GAAP Financial Measures.

Our business approach couples strong organic growth with our proven acquisition strategy. Since 2012, we have executed and successfully integrated 16 strategic acquisitions. We have a highly disciplined approach to evaluating potential acquisition targets, and have sought companies with valuable intellectual property, high aftermarket content, revenue synergies, ability to cross-sell and strong customer relationships. We operate in a highly fragmented market, which has historically provided ample acquisition targets as we look to enhance and grow our platform.

Our Industry

End Markets

We primarily compete across three core end markets of the aerospace and defense component industry: commercial, business jet and general aviation, and defense.

Commercial. The commercial aerospace market, our largest end market representing % of 2023 net sales, has experienced significant growth over the past several years as a result of increased orders for next-generation commercial aircraft and increased aftermarket requirements from higher levels of aircraft usage in a

3

Table of Contents

post-COVID environment. However, the commercial aerospace market has shown consistent long-term growth trends over the past 75 years, spurred by travel demand and the development of a global world economy. The industrys growth rate has historically outpaced global GDP growth, with RPKs increasing at an average of 1.6x global GDP growth between 1970 and 2022, reflecting an approximate 5% CAGR.

Commercial OEM revenue historically has been tied to new aircraft production, which is currently supported by the production ramp of several next-generation narrowbody aircraft programs that have large order backlogs (for example, Airbus A320 family and Boeing 737 family). These order backlogs are needed to meet the secular demand for air travel. In 2021, there were 20,675 commercial jet aircraft in service, compared to 17,712 commercial jet aircraft in service in 2010, and industry consultants project that future demand requires 34,684 commercial aircraft in service by 2032.

The commercial aftermarket has historically produced consistent revenue. In our experience, as global commercial aircraft fleets grow, maintenance requirements grow alongside them. Most maintenance requirements are recurring and non-deferrable, even during periods of economic downturn or reduced demand for commercial air travel. Given the industrys long-term secular growth trends, an increasingly larger middle class that has a high demand for travel, and a meaningfully large share of the global fleet represented by legacy aircraft, we expect continued growth and stability of our commercial aftermarket revenue.

Business Jet and General Aviation. Our second largest end market, business jet and general aviation, which accounted for approximately % of 2023 net sales, has experienced significant growth over the past several years. The emergence of several business models has provided consumers with greater accessibility and affordability to private aviation, driving increased popularity globally.

The business jet and general aviation market is comprised of all aviation operations outside of commercial and defense, and it includes both OEM and the aftermarket. This market has experienced strong demand with new asset-light fleet models, such as charter operators, jet cards and fractional jet ownership. These shared economy solutions have increased average utilization, resulting in growing demand for new aircraft. Accordingly, several modern, next-generation business jet platforms have been introduced by aircraft OEMs and production rates have been rising to meet this growing demand. Moreover, increased accessibility and affordability of private aviation has driven accelerated adoption by consumers, as flyers seek alternative options to commercial air travel, resulting in even greater flight hours and aftermarket growth.

Defense. The military aviation end market, which accounted for approximately % of 2023 net sales, has continued to benefit from growing global demand. Current geopolitical circumstances, including the Ukraine conflict, the Israeli war and the potential for engagements with China and/or Russia have resulted in increased global defense spending. We expect that defense spending will continue to increase as militaries invest to maintain operational readiness.

We believe that aftermarket and OEM demand for military aviation solutions follows global defense spending and the broader U.S. Department of Defense budget. OEM military revenue is primarily driven by spending on new aircraft platforms and systems. In an era of heightened geopolitical instability, we believe that defense spending will continue to be a priority for militaries to maintain operational readiness and invest in next-generation platforms with modern capabilities. Recently, military aftermarket revenue has been derived primarily from utilization of existing aircraft, aircraft modernization and sustainment initiatives to upgrade existing fleets and extend the service life of equipment.

Competition

The market for aerospace and defense components is highly fragmented, with few scaled competitors. As a result, we have very few direct competitors that provide the breadth of products, solutions and expertise that we are able to offer our customers. However, given the market fragmentation, we face competition from different

4

Table of Contents

competitors across individual products and applications. Competition within our product offerings range from divisions of large public corporations to small, privately held companies with singular capabilities that lack infrastructure and capacity to scale.

We compete primarily on the basis of engineering, capabilities, capacity and customer responsiveness. We believe we meet or exceed the performance and quality requirements of our customers and consistently deliver products on a timely basis with superior customer service and support. Our commitment to performance and responsiveness has allowed us to foster strong customer relationships with major aerospace and defense OEMs and Tier 1 and Tier 2 suppliers. We believe that our consistent quality, performance and breadth of capabilities are key strengths that enable us to win new business and fuel the continued long-term relationships with our customers.

Challenges

Our business is subject to a number of risks inherent to our industry, including, among others, our almost exclusive focus on the aerospace and defense industry, our ability to consummate acquisitions on satisfactory terms and to integrate effectively acquired operations and the cyclical nature of our sales to manufacturers of aircraft. Any number of these factors could impact our business, and there is no guarantee that our historical performance will be predictive of future operational and financial performance. For a description of the challenges we have faced and continue to face and the risks and limitations that could harm our prospects, see Cautionary Note Regarding Forward-Looking Statements, Summary of Risk Factors and Risk Factors included elsewhere in this prospectus.

Competitive Strengths

As a specialized supplier in the aerospace and defense component industry, we believe we are well-positioned to deliver innovative, mission-critical solutions to a wide array of aerospace and defense customers. Our key competitive strengths support our ability to offer differentiated solutions to our customers:

Portfolio of Mission-Critical, Niche Aerospace and Defense Components. We specialize in niche aerospace and defense components that are essential for the production and maintenance of aircraft and their related systems. Given the high costs typically associated with the stoppage of production or the removal of an aircraft from service, customers demand consistent reliability, performance and quality from our products. We believe that few competitors can offer the customized, high-quality solutions we provide and, as such, we believe we are the supplier of choice in the end markets in which we operate.

Intellectual Property-Driven, Proprietary Products and Expertise in an Industry with High Barriers to Entry. We derived % of our 2023 net sales from proprietary products or solutions. Our intellectual property and in-house expertise represent decades of knowledge and investment that we believe competitors would struggle to match. Furthermore, due to the industrys stringent regulatory, certification and technical requirements, the qualification process for new products is rigorous and costly. Certification processes necessitate significant time and monetary investments from both suppliers and customers, leaving little incentive for either party to repeat these processes once a product is already certified on a platform. Accordingly, we believe that these high barriers to entry provide us with additional growth opportunities with our customers, while the reliability, performance and quality of our products enhance our long-standing customer relationships.

Strategically Focused on Higher-Margin Aftermarket Content. We supply aftermarket products to a large installed, and growing, base of aircraft. We estimate that our addressable market opportunity includes more than 84,000 discrete aircraft across more than 250 total aircraft platforms. Due to our installed OEM base of proprietary products and a demanding certification process, we are often the only supplier providing these products in the aftermarket, which we generally expect to result in a recurring revenue stream for the life of each

5

Table of Contents

aircraft platform. The total life of the platforms we serve can be up to 50 years, presenting the opportunity for a long tail of aftermarket service and/or periodic replacement requirements. We believe our ability to support the full aircraft life cycle from initial build to retirement is a key differentiator and has historically generated significant revenue, as represented by the % of our 2023 net sales attributable to the aftermarket. The long-term secular growth dynamics of aftermarket demand historically have also led to higher margins and consistent revenue growth.

Highly Diversified Revenue Streams. We have strategically and purposefully constructed a highly diverse portfolio, which we believe positions us well to succeed in a variety of market conditions. Our diversified revenue base is designed to reduce our dependence on any particular product, platform, or market sector, and we believe it has been a significant factor in our resilient financial performance. The Companys diversification stretches across end markets, customers, platforms and product category or application.

| | End markets: 2023 net sales were distributed across the following basis % commercial, % business jet and general aviation, % defense and % non-aviation. |

| | Customers: No customer made up more than % of 2023 net sales. The top five customers made up % of 2023 net sales. |

| | Platforms: No aircraft platform represented more than % of 2023 net sales. The top six aircraft platforms represented less than % of total 2023 net sales. Our top two aircraft platforms are the and . |

| | Product category or application: the Companys products are utilized in a variety of applications in the interior, exterior, and engine that serve both OEM ( % of 2023 net sales) and aftermarket ( % of 2023 net sales) categories of the overall market. |

Established Business Model with a Lean, Entrepreneurial Structure. Our operations are built around a philosophy that encourages local autonomy across the Companys brands and drives entrepreneurial spirit. Critical to our success is a management structure that is designed to facilitate seamless communication across our businesses. Executive Vice Presidents are responsible for multiple brands within the Company. They support local brand leaders and also work closely with corporate management in helping to optimize potential cross-selling opportunities, operational initiatives and capital allocation. By fostering cross-communication and enabling each brand to leverage the benefits of the broader Company platform, we have created a highly scalable operational structure with few management layers. We believe our streamlined structure also facilitates efficient decision making for acquisitions and other important strategic decisions. Our streamlined leadership, coupled with a holistic approach to revenue and innovation, is intended to position us for revenue growth and ongoing operational improvements.

Disciplined and Strategic Approach to Acquisitions, with History of Successful Integration. We have a disciplined and thoughtful approach to acquisitions, as demonstrated by the successful integration of our 16 acquisitions since 2012. Our well-defined acquisition criteria have led us to target companies with proprietary products and/or processes, leading market positions, significant aftermarket potential, strong revenue synergies with potential for cross-selling and strong customer relationships. Managements experience in driving financial performance from our defined model has led to a targeted goal of doubling an acquired businesss Adjusted EBITDA over a three-to-five-year time frame post-acquisition. Our focused approach to acquisitions and the underlying drivers of value have helped create a scaled and integrated platform.

Track Record of Strong Growth, Margins and Cash Flow Generation. Since inception, we have utilized both organic and inorganic drivers to generate a portfolio of what we believe to be market leading brands and products under the Loar umbrella, enabling a consistent track record of growth and strong margins. In constructing a portfolio of capabilities that fit the needs of the marketplace, we have focused on four main strategic drivers of value in our business: launching new products, optimizing productivity, achieving value

6

Table of Contents

pricing and readying talent. By applying these drivers, we have been able to generate significant growth, high margins and high cash flow since our inception. We believe our performance-driven culture and commitment to constant improvement and execution will continue to drive strong financial performance.

For a discussion of the use of Adjusted EBITDA and Adjusted EBITDA Margin and a reconciliation to the most directly comparable GAAP measures, see Summary Financial Data.

Proven Leadership Team. Our leadership team has a depth of experience running businesses in the aerospace and defense component industry. A core group of our senior management team has worked together for over 30 years at multiple companies, and the average industry experience for 10 members of our senior leadership team is over 25 years, including having worked together for more than 15 years at the Company, McKechnie and/or TransDigm. Our management team has leveraged its extensive industry experience to construct purposely a well-designed and diversified platform at Loar, has generated significant net sales growth, and has navigated many different market environments. In addition, our management teams incentives are well-aligned with the success of Loar and its shareholders. Members of the management team and certain other key employees are expected to hold approximately % of the shares of our common stock outstanding as of , 2024, after giving effect to the Corporate Conversion and the sale of shares of common stock by us in this offering and assuming no exercise of the underwriters option to purchase additional shares. See Principal Stockholders.

Growth Strategy

Our growth strategy is made up of two key elements: (i) a value-driven operating strategy and (ii) a disciplined acquisition strategy.

Value-driven operating strategy. Our five core organic growth value drivers are:

| | Providing highly engineered, value-additive solutions to our customers: We are well positioned in our core underlying markets to benefit from the aerospace and defense component industrys long-term secular growth trends. Our proprietary products and consistent ability to meet customer needs have resulted in strong, long-standing customer relationships. Our quality and breadth of offerings have |

7

Table of Contents

| enabled us to maintain established positions on nearly every major aircraft platform such that we benefit from both large production backlogs for new aircraft as well as the aftermarket requirements associated with aircraft in use today. We expect to maintain entrenched positions for the life of the majority of these aircraft platforms due in part to high switching costs and significant barriers to entry. When coupled with the long tail of aftermarket requirements, our positioning creates a favorable mix of business with highly profitable opportunities. |

| | Value-based pricing opportunities: Historically we have been able to realize a sustainable pricing strategy reflective of the value of our products position in the supply chain. We believe our business model creates value-based pricing opportunities through a compelling combination of attributes. Proprietary products, customized designs, superior quality, the relative low cost of our solutions compared to the total cost of the aircraft platform, and high switching costs are among the attributes that we believe lead our customers to prioritize performance and reliability over price. |

| | Winning profitable new business: We have won profitable new business from existing customers, and we have expanded our customer base through new relationships, by leveraging our broad capabilities, extensive engineering expertise and reputation for quality and performance. By successfully meeting customers design requirements, certification needs and/or timing constraints, we have garnered trust with customers and created cross-selling opportunities across various platforms, systems and customers. Our new business pipeline targets opportunities within attractive aircraft programs where we see an opportunity to leverage customer relationships or product overlaps and drive new, profitable revenue streams. |

| | New product introductions: We continuously develop new innovative solutions for our customers. Our product development strategy has been guided by our strong understanding of our customers needs, which is driven by the open and candid relationships we foster. We seek to introduce new products that not only address critical customer needs, but also serve large addressable fleets with aftermarket requirements. Additionally, as customers continue to navigate an increasingly complex supply chain, we believe they are focused on working with a smaller set of reliable core suppliers. As a supplier of a broad suite of high-quality, niche solutions that serve a broad range of applications, we are well-positioned to benefit from customers desire for a more streamlined supply chain. |

| | Driving operational efficiencies that improve cost structure and profitability: We are focused on consistent operational improvements to our cost structure that we believe will drive profitability. We frequently review opportunities for margin enhancement through key operational metrics, productivity initiatives, management directives and weekly or quarterly reviews to drive operational efficiencies. Additionally, we expect our margins and profitability to improve from focused growth strategies that provide high contribution margins and value-based pricing that, at a minimum, achieve price increases greater than inflation. |

Disciplined acquisition strategy. Acquisitions are a core element of our long-term growth strategy. We have considerable experience in executing acquisitions and integrating acquired businesses into our Company and culture, having done so 16 times since our formation in 2012. Our disciplined acquisition strategy revolves around acquiring aerospace and defense component businesses with significant aftermarket potential and proprietary content and/or processes, where we believe there is a clear path to value creation.

The aerospace supply chain is highly fragmented, with many components supplied by smaller privately-owned businesses that, in turn, sell to system integrators, Tier 1 or Tier 2 manufacturers, or large OEM participants. We believe there is a significant opportunity for further consolidation of the supply chain. We have maintained a robust pipeline of acquisition targets and are often in active discussions with business owners that recognize our established culture and the opportunity for them to leverage the Companys existing infrastructure, customer base, platform exposure and industry relationships. We are positioned as an acquirer of choice due to our entrepreneurial philosophy and desire to further grow and improve each brand we acquire, based on a flexible

8

Table of Contents

post-acquisition integration that suits each businesss specific strengths and culture. We intentionally maintain each acquired businesss brand to preserve long-term customer relationships and capture revenue synergies.

As part of our acquisition strategy, we take a disciplined approach to acquisition target screening, focusing on identifying key characteristics that we believe provide insight on strategic fit. Such characteristics include: (i) aerospace- and defense-focused businesses; (ii) proprietary content and/or processes; (iii) significant aftermarket exposure or potential to grow; (iv) focus on niche markets or products with strong market positions; (v) capabilities where the opportunity to cross-sell our existing portfolio of products exists; and (vi) long-standing customer relationships. Our disciplined approach to acquisitions has allowed us to be opportunistic, which has built the Company into a leading aerospace and defense component supplier.

Summary of Risk Factors

Investing in our common stock involves a high degree of risk. You should carefully consider all of the risks described in Risk Factors before deciding to invest in our common stock. If any of the risks actually occurs, our business, results of operations, prospects, and financial condition may be materially adversely affected. In such case, the trading price of our common stock may decline and you may lose part or all of your investment. Below is a summary of some of the principal risks we face:

| | our business focuses almost exclusively on the aerospace and defense industry; |

| | we rely heavily on certain customers for a significant portion of our sales; |

| | we have in the past consummated acquisitions and intend to continue to pursue acquisitions, and our business may be adversely affected if we cannot consummate acquisitions on satisfactory terms, or if we cannot effectively integrate acquired operations; |

| | we depend on our executive officers, senior management team and highly trained employees and any work stoppage, difficulty hiring similar employees, or ineffective succession planning could adversely affect our business; |

| | our sales to manufacturers of aircraft are cyclical, and a downturn in sales to these manufacturers may adversely affect us; |

| | our business depends on the availability and pricing of certain components and raw materials from suppliers; |

| | our operations depend on our manufacturing facilities, which are subject to physical and other risks that could disrupt production; |

| | our business may be adversely affected if we were to lose our government or industry approvals, if more stringent government regulations were enacted or if industry oversight were to increase; |

| | our commercial business is sensitive to the number of flight hours that our customers planes spend aloft, the size and age of the worldwide aircraft fleet and our customers profitability, and these items are, in turn, affected by general economic and geopolitical and other worldwide conditions; |

| | technology failures or cyber security breaches or other unauthorized access to our information technology systems or sensitive or proprietary information could have an adverse effect on the Companys business and operations; |

| | our inability to adequately enforce and protect our intellectual property or defend against assertions of infringement could prevent or restrict our ability to compete; |

| | we could incur substantial costs as a result of violations of or liabilities under environmental laws and regulations; |

| | tariffs on certain imports to the United States and other potential changes to U.S. tariff and import/export regulations may have a negative effect on global economic conditions and our business, financial results and financial condition; |

9

Table of Contents

| | our indebtedness, which is subject to variable interest rates, could adversely affect our financial health and could harm our ability to react to changes to our business; |

| | to service our indebtedness, we will require a significant amount of cash, and our ability to generate cash depends on many factors beyond our control, and any failure to meet our debt service obligations could harm our business, financial condition and results of operations; and |

| | the other factors discussed under Risk Factors. |

Implications of Being an Emerging Growth Company

We qualify as an emerging growth company as defined in Section 2(a)(19) of the Securities Act. As a result, we are permitted to, and intend to, rely on exemptions from certain disclosure requirements that are applicable to other companies that are not emerging growth companies. Accordingly, in this prospectus, we (i) have presented only two years of audited financial statements; and (ii) have not included a compensation discussion and analysis of our executive compensation programs. In addition, for so long as we are an emerging growth company, among other exemptions, we will:

| | not be required to engage an independent registered public accounting firm to report on our internal controls over financial reporting pursuant to Section 404(b) of the Sarbanes-Oxley Act; |

| | not be required to comply with the requirement in Public Company Accounting Oversight Board Auditing Standard 3101, The Auditors Report on an Audit of Financial Statements When the Auditor Expresses an Unqualified Opinion, to communicate critical audit matters in the auditors report; |

| | be permitted to present only two years of audited financial statements and only two years of related Managements Discussion and Analysis of Financial Condition and Results of Operations in our periodic reports and registration statements, including in this prospectus; |

| | not be required to disclose certain executive compensation-related items such as the correlation between executive compensation and performance and comparisons of the chief executive officers compensation to median employee compensation; or |

| | not be required to submit certain executive compensation matters to stockholder advisory votes, such as say-on-pay, say-on-frequency, and say-on-golden parachutes. |

We will remain an emerging growth company until the earliest to occur of:

| | our reporting of $1.235 billion or more in annual gross revenue; |

| | our becoming a large accelerated filer, with at least $700 million of equity securities held by non-affiliates; |

| | our issuance, in any three-year period, of more than $1.0 billion in non-convertible debt; and |

| | the fiscal year end following the fifth anniversary of the completion of this initial public offering. |

The Jumpstart Our Business Startups Act of 2012 (the JOBS Act), also permits an emerging growth company such as us to take advantage of an extended transition period to comply with new or revised accounting standards applicable to public companies. We have elected to use this extended transition period under the JOBS Act.

Our Corporate Information

We currently operate as a Delaware limited liability company under the name Loar Holdings, LLC, which is a holding company that holds all of the equity interests of Loar Group Inc., the entity which directly and indirectly holds all of the equity interests in our operating subsidiaries. Loar Holdings, LLC was formed

10

Table of Contents

August 21, 2017. Prior to the effectiveness of the registration statement of which this prospectus forms a part, Loar Holdings, LLC will convert into a Delaware corporation pursuant to a statutory conversion and will change its name to Loar Holdings Inc.

The purpose of the Corporate Conversion is to reorganize our structure so that the entity that is offering our common stock to the public in this offering is a corporation rather than a limited liability company and so that our existing investors will own our common stock rather than equity interests in a limited liability company. For more information, see Corporate Conversion.

Our principal offices are located at 20 New King Street, White Plains, New York 10604. Our telephone number is 914-909-1311. We maintain a website at loargroup.com. The reference to our website is intended to be an inactive textual reference only. The information contained on, or that can be accessed through, our website is not part of this prospectus.

Simplified Ownership Structure

The diagram below depicts our organizational structure and ownership after giving effect to the Corporate Conversion and this offering, excluding certain dormant or inactive entities. Each of our subsidiaries is wholly-owned by its immediate parent. For more information, see Corporate Conversion and Principal Stockholders.

11

Table of Contents

THE OFFERING

| Issuer |

Loar Holdings Inc. |

| Common stock offered by us |

(or shares if the underwriters exercise their option to purchase additional shares of common stock in full). |

| Option to purchase additional shares of our common stock |

We have granted the underwriters a 30-day option from the date of this prospectus to purchase up to additional shares of our common stock at the initial public offering price, less underwriting discounts, and commissions. |

| Common stock to be outstanding immediately after this offering |

shares (or shares if the underwriters exercise their option to purchase additional shares of common stock in full ). |

| Use of proceeds |

We estimate that the net proceeds to us from this offering will be approximately $ million (or approximately $ million, if the underwriters exercise their option to purchase additional shares of common stock in full), assuming an initial public offering price of $ per share, which is the mid-point of the estimated price range set forth on the cover page of this prospectus, and after deducting the estimated underwriting discounts and commissions and estimated offering expenses payable by us. For a sensitivity analysis as to the offering price and other information, see Use of Proceeds. |

| We intend to use the net proceeds to us from this offering for . See Use of Proceeds. |

| Dividend policy |

We have no current plans to pay dividends on our common stock. Any decision to declare and pay dividends in the future will be made at the sole discretion of our Board and will depend on, among other things, our results of operations, cash requirements, financial condition, legal, tax, regulatory, and contractual restrictions, including restrictions in the agreements governing our indebtedness, and other factors that our Board may deem relevant. See Dividend Policy. |

| Risk factors |

Investing in shares of our common stock involves a high degree of risk. See Risk Factors beginning on page 18 for a discussion of factors you should carefully consider before investing in shares of our common stock. |

| Proposed trading symbol |

LOAR. |

The number of shares of common stock to be outstanding following this offering is based on shares of common stock outstanding as of after giving effect to the Corporate Conversion, and excludes shares of our common stock reserved for future issuance under our new long-term incentive

12

Table of Contents

plan (the LTIP), which will become effective on the day prior to the first public trading date of our common stock, as well as any future increases in the number of shares of our common stock reserved for issuance under our LTIP.

Unless we indicate otherwise or the context otherwise requires, this prospectus reflects and assumes:

| | the completion of the Corporate Conversion; |

| | the filing and effectiveness of our certificate of incorporation and the adoption of our bylaws immediately prior to the consummation of this offering; |

| | no exercise by the underwriters of their option to purchase additional shares of our common stock; and |

| | an initial public offering price of $ per share of our common stock, which is the mid-point of the estimated price range set forth on the cover page of this prospectus. |

13

Table of Contents

SUMMARY FINANCIAL DATA

The following tables summarize our consolidated financial data. The summary consolidated statements of operations and cash flows data for the years ended December 31, 2022 and 2023 and the consolidated balance sheets data as of December 31, 2022 and 2023 are derived from our audited consolidated financial statements that are included elsewhere in this prospectus. The summary consolidated financial data in this section are not intended to replace the consolidated financial statements and related notes thereto included elsewhere in this prospectus and are qualified in their entirety by the consolidated financial statements and related notes thereto included elsewhere in this prospectus.

Our historical results are not necessarily indicative of the results that may be expected in the future. You should read the summary historical financial data below in conjunction with the section titled Managements Discussion and Analysis of Financial Condition and Results of Operations and the financial statements and related notes included elsewhere in this prospectus.

| Years Ended December 31, | ||||||||

| 2022 | 2023 | |||||||

| Statements of Operations Data (in thousands): |

||||||||

| Net sales |

$ | 239,434 | ||||||

| Cost of sales |

127,934 | |||||||

| Gross profit |

111,500 | |||||||

| Selling, general and administrative expenses |

66,536 | |||||||

| Transaction expenses |

6,365 | |||||||

| Other income |

861 | |||||||

|

|

|

|||||||

| Operating income |

39,460 | |||||||

| Interest expense, net |

42,071 | |||||||

|

|

|

|||||||

| Loss before income taxes |

(2,611 | ) | ||||||

| Income tax benefit |

142 | |||||||

|

|

|

|||||||

| Net loss |

$ | (2,469 | ) | |||||

|

|

|

|||||||

| Basic and Diluted Net Loss per Common Unit: |

||||||||

| Net loss per common unit |

$ | (12,101.03 | ) | |||||

| Weighted-average number of common units outstanding |

204 | |||||||

| Other Financial Data (in thousands except as noted): |

||||||||

| Cash flows provided by (used in): |

||||||||

| Operating activities |

$ | 13,270 | ||||||

| Investing activities |

(181,833 | ) | ||||||

| Financing activities |

135,305 | |||||||

| Depreciation |

8,882 | |||||||

| Amortization of intangible and other long-term assets |

25,074 | |||||||

| Capital expenditures |

(7,934 | ) | ||||||

| Payment for acquisitions, net of cash acquired |

(173,899 | ) | ||||||

| EBITDA (1) |

73,416 | |||||||

| Adjusted EBITDA (1) |

83,273 | |||||||

| Net loss margin |

(1.0% | ) | ||||||

| Adjusted EBITDA Margin (1) |

34.8% | |||||||

| (1) | References to EBITDA mean earnings before interest, taxes, depreciation and amortization, references to Adjusted EBITDA mean EBITDA plus, as applicable for each relevant period, certain adjustments as set forth in the reconciliations of net loss to EBITDA and Adjusted EBITDA, and references to Adjusted |

14

Table of Contents

| EBITDA Margin refer to Adjusted EBITDA divided by net sales. EBITDA, Adjusted EBITDA and Adjusted EBITDA Margin are not measurements of financial performance under U.S. GAAP. We present EBITDA, Adjusted EBITDA and Adjusted EBITDA Margin because we believe they are useful indicators for evaluating operating performance. In addition, our management uses Adjusted EBITDA to review and assess the performance of the management team in connection with employee incentive programs and to prepare its annual budget and financial projections. Moreover, our management uses Adjusted EBITDA of target companies to evaluate acquisitions. EBITDA, Adjusted EBITDA and Adjusted EBITDA Margin should not be considered in isolation of, or as an alternative to, measures prepared in accordance with GAAP. There are a number of limitations related to the uses of EBITDA, Adjusted EBITDA and Adjusted EBITDA Margin in lieu of net loss, which is the most directly comparable financial measure calculated in accordance with GAAP. Our uses of the terms EBITDA, Adjusted EBITDA and Adjusted EBITDA Margin may vary from the uses of similar terms by other companies in our industry and accordingly may not be comparable to similarly titled measures used by other companies. EBITDA, Adjusted EBITDA and Adjusted EBITDA Margin are reconciled as follows (in thousands): |

| Years Ended December 31, | ||||||||

| 2022 | 2023 | |||||||

| Net loss |

$ | (2,469 | ) | |||||

| Adjustments: |

||||||||

| Interest expense, net |

42,071 | |||||||

| Income tax benefit |

(142 | ) | ||||||

|

|

|

|||||||

| Operating income |

39,460 | |||||||

| Depreciation |

8,882 | |||||||

| Amortization |

25,074 | |||||||

|

|

|

|||||||

| EBITDA |

73,416 | |||||||

| Adjustments: |

||||||||

| Recognition of inventory step-up (a) |

704 | |||||||

| Other income (b) |

(861 | ) | ||||||

| Transaction expense (c) |

6,365 | |||||||

| Stock-based compensation (d) |

1,526 | |||||||

| Acquisition integration costs (e) |

1,913 | |||||||

| COVID-19-related expenses (f) |

210 | |||||||

|

|

|

|||||||

| Adjusted EBITDA |

$ | 83,273 | ||||||

|

|

|

|||||||

| Net sales |

$ | 239,434 | ||||||

| Net loss margin |

(1.0 | %) | ||||||

| Adjusted EBITDA Margin |

34.8 | % | ||||||

| (a) | Represents accounting adjustments to inventory associated with acquisitions of businesses that were charged to cost of sales when inventory was sold. |

| (b) | Represents a grant from the U.S. Department of Transportation under the Aviation Manufacturing Jobs Protection Program (AMJP). |

| (c) | Represents transaction-related costs for acquisitions comprising deal fees, legal, financial and tax due diligence expenses, and valuation costs that are required to be expensed as incurred. |

| (d) | Represents the non-cash compensation expense recognized by the Company for our restricted equity unit awards. |

| (e) | Represents costs incurred to integrate acquired businesses and product lines into Loars operations, facility relocation costs and other acquisition-related costs. |

| (f) | Represents incremental costs related to the pandemic that are not expected to recur once the pandemic dissipates and are clearly separable from normal operations (for example, additional cleaning and disinfecting of facilities by contractors above and beyond normal requirements and COVID sick pay). |

15

Table of Contents

The following table sets forth a reconciliation of net loss to EBITDA, Adjusted EBITDA and Adjusted EBITDA Margin for the time periods indicated (in thousands unless otherwise indicated):

| Year Ended | Twelve Months Ended Dec. 31, 2017 (1) |

Oct. 2, 2017 through Dec. 31, 2017 (1) |

Jan. 1, 2017 through Oct. 1, 2017 (1) |

Year Ended | ||||||||||||||||||||||||||||||||||||||||||||

| Dec. 31, 2021 |

Dec. 31, 2020 |

Dec. 31, 2019 |

Dec. 31, 2018 |

Dec. 31, 2016 |

Dec. 31, 2015 |

Dec. 31, 2014 |

Dec. 31, 2013 |

Dec. 31, 2012 |

||||||||||||||||||||||||||||||||||||||||

| (Successor) | (Predecessor) | |||||||||||||||||||||||||||||||||||||||||||||||

| Net loss |

$ | (5,354 | ) | $ | (17,052 | ) | $ | (4,152 | ) | $ | (5,721 | ) | $ | (7,063 | ) | $ | (3,409 | ) | $ | (3,654 | ) | $ | (122 | ) | $ | 1,278 | $ | 6,075 | $ | (1,058 | ) | $ | (2,404 | ) | ||||||||||||||

| Adjustments: |

||||||||||||||||||||||||||||||||||||||||||||||||

| Income tax provision (benefit) |

(2,599 | ) | (2,147 | ) | 774 | (1,101 | ) | (13,228 | ) | (12,414 | ) | (814 | ) | 499 | 685 | (2,382 | ) | 105 | 160 | |||||||||||||||||||||||||||||

| Interest expense, net |

31,637 | 32,864 | 29,304 | 16,846 | 10,610 | 3,817 | 6,793 | 8,933 | 981 | 15 | 10 | 14 | ||||||||||||||||||||||||||||||||||||

| Loss on extinguishment of debt (a) |

| | | | 5,233 | | 5,233 | | | | | | ||||||||||||||||||||||||||||||||||||

| Foreign exchange gain (b) |

| | | | | | | (72 | ) | | | | | |||||||||||||||||||||||||||||||||||

| Gain on insurance recoveries (c) |

| | | | | | | | | (150 | ) | | | |||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

| Operating income (loss) |

23,684 | 13,665 | 25,926 | 10,024 | (4,448 | ) | (12,006 | ) | 7,558 | 9,238 | 2,944 | 3,558 | (943 | ) | (2,230 | ) | ||||||||||||||||||||||||||||||||

| Depreciation |

9,143 | 8,622 | 7,879 | 7,256 | 5,390 | 1,937 | 3,453 | 5,073 | 2,163 | 2,028 | 1,416 | 399 | ||||||||||||||||||||||||||||||||||||

| Amortization |

23,550 | 22,429 | 21,919 | 16,405 | 8,399 | 4,613 | 3,786 | 4,795 | 1,246 | 906 | 1,385 | 817 | ||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

| EBITDA |

56,377 | 44,716 | 55,724 | 33,685 | 9,341 | (5,456 | ) | 14,797 | 19,106 | 6,353 | 6,492 | 1,858 | (1,014 | ) | ||||||||||||||||||||||||||||||||||

| Adjustments: |

||||||||||||||||||||||||||||||||||||||||||||||||

| Recognition of inventory step-up (d) |

740 | 3,241 | 2,001 | 1,162 | 6,929 | 6,441 | 488 | 1,385 | 414 | 160 | 666 | 1,341 | ||||||||||||||||||||||||||||||||||||

| Other (income) loss (e) |

396 | (1,663 | ) | | (3,521 | ) | 2,313 | | 2,313 | (500 | ) | | | | | |||||||||||||||||||||||||||||||||

| Transaction expenses (f) |

804 | 2,001 | 2,811 | 2,135 | 10,074 | 7,482 | 2,592 | 1,416 | 1,840 | | 688 | 664 | ||||||||||||||||||||||||||||||||||||

| Stock-based compensation (g) |

1,686 | 1,686 | 1,686 | 1,665 | 934 | 381 | 553 | 247 | 189 | 189 | 166 | 101 | ||||||||||||||||||||||||||||||||||||

| Acquisition integration costs (h) |

642 | 405 | 931 | 2,406 | 1,101 | 288 | 813 | 197 | 451 | 21 | 21 | | ||||||||||||||||||||||||||||||||||||

| COVID-19 related expenses (i) |

147 | 399 | | | | | | | | | | | ||||||||||||||||||||||||||||||||||||

| Management service agreement fees and expenses (j) |

| | | | 843 | | 843 | 1,157 | 616 | 567 | 454 | 554 | ||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

| Adjusted EBITDA |

$ | 60,792 | $ | 50,785 | $ | 63,153 | $ | 37,532 | $ | 31,535 | $ | 9,136 | $ | 22,399 | $ | 23,008 | $ | 9,863 | $ | 7,429 | $ | 3,853 | $ | 1,646 | ||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

| Net sales |

$ | 188,897 | $ | 164,564 | $ | 182,623 | $ | 112,572 | $ | 94,346 | $ | 26,179 | $ | 68,167 | $ | 75,780 | $ | 42,371 | $ | 39,240 | $ | 22,983 | $ | 8,923 | ||||||||||||||||||||||||

| Net loss margin |

(2.8 | %) | (10.4 | %) | (2.3 | %) | (5.1 | %) | (7.5 | %) | (13.0 | %) | (5.4 | %) | (0.2 | %) | 3.0 | % | 15.5 | % | (4.6 | %) | (26.9 | %) | ||||||||||||||||||||||||

| Adjusted EBITDA Margin |

32.2 | % | 30.9 | % | 34.6 | % | 33.3 | % | 33.4 | % | 34.9 | % | 32.9 | % | 30.4 | % | 23.3 | % | 18.9 | % | 16.8 | % | 18.4 | % | ||||||||||||||||||||||||

| (1) | For the period January 1, 2017 through October 1, 2017 (Predecessor Period), the Company is referred to as the Predecessor. For the period October 2, 2017 through December 31, 2017 (Successor Period), the Company is referred to as Successor. The Company applied pushdown accounting to the transaction. Due to the application of push-down accounting, different bases of accounting have been used to prepare the consolidated financial statements in the Predecessor Period and Successor Period. A black line separates the Predecessor Period and Successor Period to highlight the lack of comparability between these two bases of accounting. The Successor Period includes the accounts of Loar Holdings, LLC and its subsidiaries. The Predecessor Period includes the accounts of Loar Group, Inc. Intercompany accounts and transactions between consolidated entities have been eliminated. |

| (a) | Represents the write-off of unamortized debt issuance costs associated with the extinguishment of debt. |

| (b) | Represents foreign exchange gains related to an overseas distribution center. |

| (c) | Represents insurance proceeds on property losses. |

| (d) | Represents accounting adjustments to inventory associated with acquisitions of businesses that were charged to cost of sales when inventory was sold. |

| (e) | Amounts represent income or losses not related to operations. The impact for the year ended December 31, 2021 represented certain long-lived asset write-offs of $1.4 million, partially offset by a government grant of $1.0 million. The impact for the year ended December 31, 2020 represented a government grant and a gain on sale of assets of $1.0 million and $0.7 million, respectively. The impact for the year ended December 31, 2018 is primarily attributable to contingent consideration payments for performance targets achieved post-acquisition. The impact for the 10 months ended October 1, 2017 represented an impairment of certain long-lived assets. The impact for the year ended December 31, 2016 represented a reversal of accrued contingency consideration related to unmet performance targets post-acquisition. |

| (f) | Represents transaction-related costs for acquisitions comprising deal fees, legal, financial and tax due diligence expenses, and valuation costs that are required to be expensed as incurred. |

| (g) | Represents the non-cash compensation expense recognized by the Company for restricted equity unit awards. |

| (h) | Represents costs incurred to integrate acquired businesses and product lines into Loars operations, facility relocation costs and other acquisition-related costs. |

| (i) | Represents incremental costs related to the pandemic that are not expected to recur once the pandemic dissipates and are clearly separable from normal operations (for example, additional cleaning and disinfecting of facilities by contractors above and beyond normal requirements and COVID sick pay). |

| (j) | Management service agreement fees and expenses paid to former owner. |

16

Table of Contents

| Pro Forma Per Share Data (2): |

||||

| Pro Forma net income (loss) per share: |

||||

| Basic |

||||

| Diluted |

||||

| Pro Forma weighted-average shares used in computing net income (loss) per share: |

||||

| Basic |

||||

| Diluted |